Every new client, insurer, or funding structure adds a layer. For banks running receivables and payables finance portfolios, those layers become the problem faster than you think.

Receivables finance programs rarely fail because of a bad deal. They stall and can eventually break because the operating model underneath them was never built to scale.

As banks grow their AR portfolios across clients, regions, funding structures and insurer relationships, friction compounds beneath the surface. Onboarding a new enterprise client brings its own insurance structure, approval hierarchy and limit logic. A new regional program means a new set of validation rules. A new capital participant adds another reconciliation touchpoint. Each addition feels manageable in isolation, but across 10 programs spanning multiple geographies, it no longer is.

The result is predictable. Operational exceptions multiply faster than the deals generating them, onboarding timelines stretch, and analyst capacity gets absorbed by reconciliation work that adds no strategic value while creating blind spots where risk accumulates and decision-makers lose confidence.

Program-by-Program Oversight Doesn’t Scale

The core challenge for banks scaling receivables finance is that most operational models were designed for individual programs, not portfolios.

When limit enforcement lives at the program level, concentration can build across parallel client structures without triggering a single alert; when onboarding logic isn’t standardized, each new client effectively rebuilds the control framework from scratch; when exposure definitions vary by program and risk takers use multiple insurance policy structures and syndications, consolidated portfolio views require manual reconciliation and are always a step behind.

The Bank for International Settlements1 has flagged the structural dimension of this challenge directly: as banks’ linkages with non-bank financial intermediaries deepen, the ability to aggregate and monitor exposures across structures becomes both a supervisory and operational imperative. Without unified exposure frameworks, risk accumulates invisibly across programs and participants.

What Portfolio-Level Control Actually Looks Like for Banks

Scaling receivables finance with efficiency requires three things working together:

- Standardized workflows across client structures. Exposure definitions normalized at intake. Limit logic applied consistently across all client programs, not rebuilt independently for each one. Exception management automated where risk is low, so credit and operations teams focus on decisions that actually require judgment.

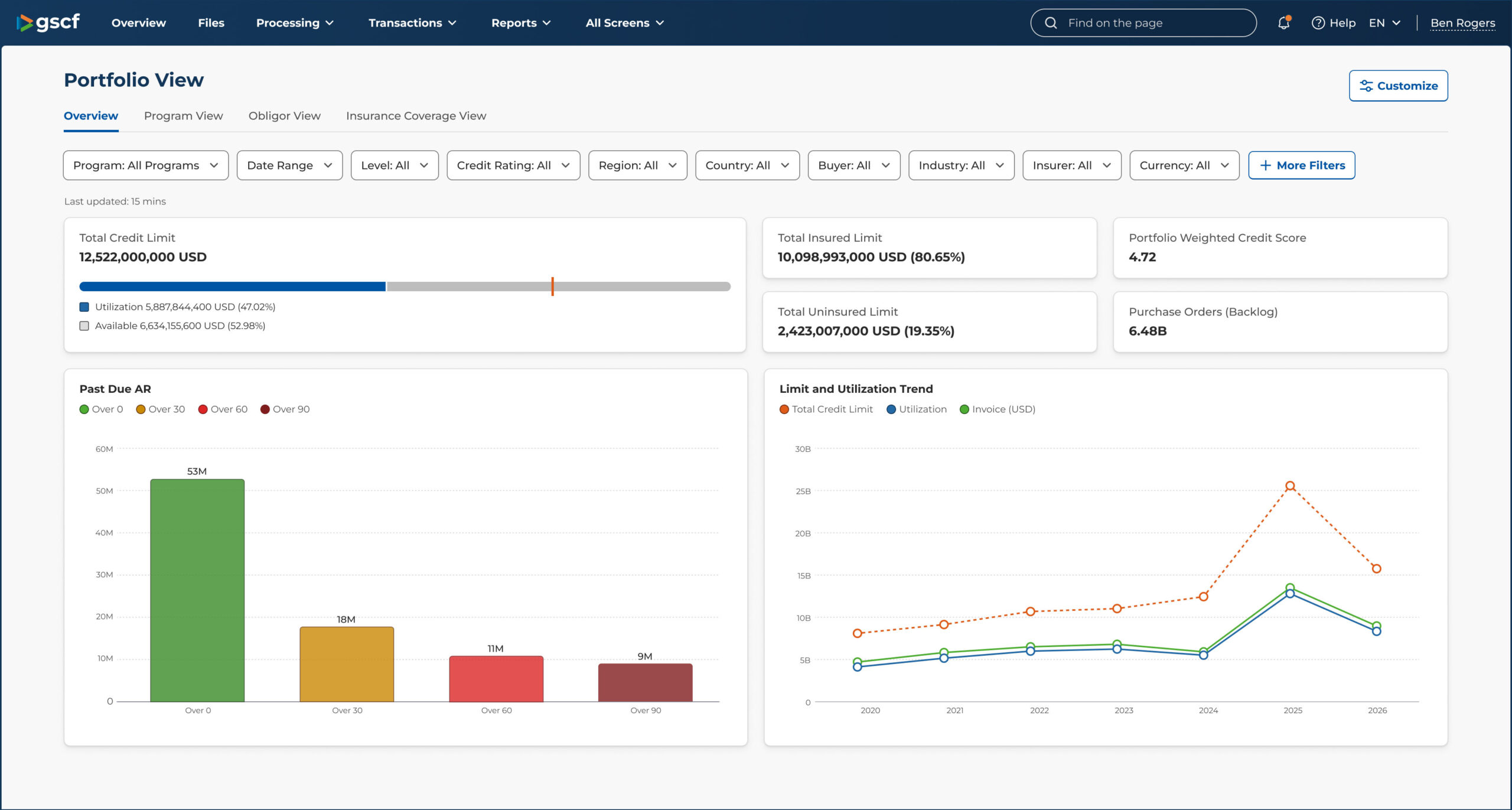

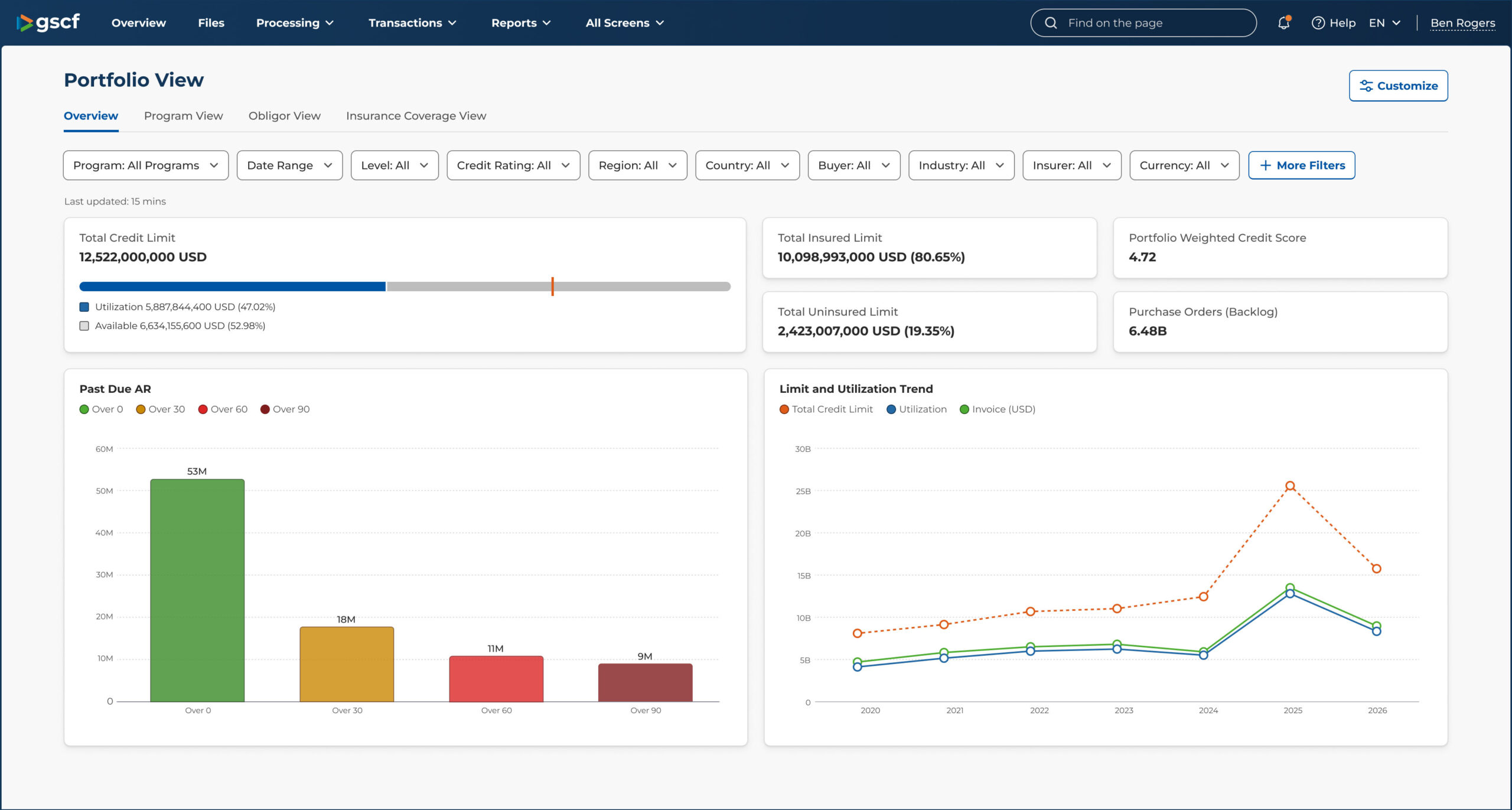

- Consolidated obligor visibility across programs, regions, and insurers. A single obligor appearing across three regional client programs may look within threshold in each and well above it in aggregate. That aggregation has to work across the full operating reality: group entities and geographies; country and political risk based on where trading actually happens; parental guarantees that change the credit picture; and the bank’s existing exposures to the same client across different financing structures and regional systems. Without seamless consolidation across those dimensions, true client and obligor risk stays fragmented and concentration breaches remain hidden until they surface in committee. With it, exposure is identified early and limit adjustments happen before thresholds are crossed.

- Embedded decisioning, not periodic reporting. Reporting tells you what happened. Embedded decisioning changes what happens next. When concentration alerts trigger automatically before thresholds are approached, when a limit increase request can be validated against consolidated obligor exposure in minutes rather than days, origination teams move faster and with greater confidence. For banks competing on responsiveness, that difference is measurable.

From Program Management to Portfolio Control

GSCF’s C4: Connected Capital Control Center was built specifically for this transition – from program-by-program oversight to true portfolio management across a bank’s receivables finance book.

Because GSCF manages the platform on behalf of banks and their corporate clients, the operational complexity sits with us, not with the bank’s internal teams. Banks get the portfolio-level visibility and control they need without taking on the servicing burden of managing it themselves. C4’s platform core capabilities include:

- Aggregated obligor exposure visibility across client programs, funders and counterparties, with normalized exposure definitions and built-in limit management and automated concentration controls

- Insured vs. retained vs participated exposure visibility across co-originated and participated positions

- Standardized global workflows with structured exception management

- A purpose-built control platform to handle structural complexity with standardized workflows, granular controls and a full audit trail for every change without needing to define workarounds

- Portfolio-level reporting and embedded decisioning that scale across regions and structures

The result: new client programs scale within established parameters. Onboarding timelines compress. Cost-to-serve doesn’t rise proportionally with volume. And when a client requests incremental capacity or a new region is added, credit teams can validate impact against consolidated portfolio exposure and respond faster, a competitive advantage in a market where deal speed matters.

See It in Practice

The use case below shows how one bank made this transition – moving from program-by-program reporting to true portfolio-level oversight, and what that meant for their trade finance and credit teams day-to-day.

A few of the questions it addresses:

- How do you get real-time insight into obligor exposure across client programs, insurers and geographies?

- How do you embed credit limits, concentration thresholds and automated alerts directly into operations so governance scales with portfolio growth?

- How do you onboard new AR programs without rebuilding operational workflows each time?

GSCF’s C4: Connected Capital Control Center is our next-generation servicing platform purpose-built to help banks, asset managers and enterprise corporates originate, manage and analyze working capital programs with greater visibility, control and confidence. Learn more at www.gscf.com.1 Basel Committee on Banking Supervision, Banks’ interconnections with non-bank financial intermediaries, BIS, July 2025. https://www.bis.org/bcbs/publ/d598.pdf